Table of Content

This is in spite of not having to come to the closing table with a down payment, which many in the past said the lack of a down payment on loan programs helped destabilize the mortgage market in the last decade. Yet veteran borrowers are a responsible group and they show that responsibility every month when they write the check for the mortgage payment. The Oregon Veteran Home Loan Program offers eligible veterans fixed-rate financing for owner-occupied, single-family residences in Oregon. The veteran home loan product is a non-expiring, lifetime benefit for any eligible Oregon veteran and may be used up to four times.

The term of the loan may be for as long as 30 years and 32 days. No loan can be guaranteed by VA without first being appraised by a VA-assigned fee appraiser. The Veteran borrower typically pays for the appraisal upon completion, according to a fee schedule approved by VA. It is not an inspection and does not guarantee the house is free of defects.

If you have remaining entitlement, you do have a home loan limit

A distinct advantage of using your VA loan is that you may not have to pay some of the additional fees normally paid at... Many borrowers get their COEs and scratch their heads because it says that their entitlement is only $36,000. An experienced VA loan officer can calculate your entitlement for loans above this amount. Most borrowers with full entitlement intact will have an additional $68,250 of VA backing available.

Deed-in-Lieu of Foreclosure – The borrower voluntarily agrees to deed the property to the servicer instead of going through a lengthy foreclosure process. Short Sale – When the servicer agrees to allow a borrower to sell his/her home for a lesser amount than what is currently required to pay off the loan. Additional time to arrange a private sale – The servicer agrees to delay foreclosure to allow a sale to close if the loan will be paid off. Loan Modification – Provides the borrower a fresh start by adding the delinquency to the loan balance and establishing a new payment schedule. Special Forbearance – The servicer agrees not to initiate foreclosure to allow time for borrowers to repay the missed installments. An example of when this would be likely is when a borrower is waiting for a tax refund.

Get help from Veterans Crisis Line

A VA guaranteed home loan offers a number of safeguards and advantages over a non VA guaranteed loan. For example, the interest rate is competitive with conventional rates with little or no down payment required. A VA guaranteed home loan is made by private lenders, such as banks, savings and loan associations, and mortgage companies.

Instead, it means that if you default on a loan that’s under $144,000, we guarantee to your lender that we’ll pay them up to $36,000. For loans over $144,000, we guarantee to your lender that we’ll pay up to 25% of the loan amount. Individuals who completed less than 6 years may be eligible if discharged for a service-connected disability.

VA Home Loans

The amounts may vary depending on the size of the loan and location of the property. VA does not have the authority to take a second-lien position on a property. In the case of disaster, the Secretary may guarantee a loan whether or not it is a second lien through a public entity providing disaster assistance. The borrower obtaining a loan may only be charged closing costs allowed by VA. How to secure a VA loan and all of the benefits that go along with it in an easy, step by step guide for active duty...

The guarantee is in favor of the lender but is paid for by the borrower in the form of a mortgage insurance policy. A mortgage insurance policy doesn’t cover making monthly payments should the borrowers be unable to pay for some reason but does provide the lender with some compensation should the loan ever go into foreclosure. This mortgage insurance policy is simply referred to by lenders as the VA Home Loan Guarantee and is financed by what is known as the Funding Fee. There are several reasons why VA approved mortgage lenders appreciate VA home loan applicants. Such lenders appreciate their service to their country and do what they can in return.

Guaranty Remittance Overview

The builder of a new home is required to give the purchasing Veteran either a one-year warranty or a 10-year insurance-backed protection plan. Repayment Plan – The borrower makes a regular installment each month plus part of the missed installments. Certain medical conditions, or service-connected disability.

This translates to a maximum loan amount of $1,094,625 for 2010. It doesn’t guarantee the borrowers will get approved for a VA loan. The VA home loan for a purchase requires a decent credit history and the lender will pull a credit report and request credit scores. While the VA doesn’t issue guidelines regarding a minimum credit score, VA lenders do, typically around 620 or as low as 600. The Oregon Department of Veterans’ Affairs will increase the maximum loan limit for the Oregon Veteran Home Loan for 2023, conforming to loan limits for mortgages set by the Federal Housing Finance Agency .

The percentage depends on whether a borrower makes a down payment. Most VA loans are obtained without a down payment; therefore, most VA loans receive 25% backing by the federal government. The conforming loan limit for most U.S. counties is $417,000. And, the VA is willing to back up to 25% of all VA loans up to this limit.

Under the VA-guaranteed Home Loan program, VA does not make the loan to you. The guaranty amount is what VA would pay a lender should your loan go into foreclosure, deed-in-lieu, or short-sale. VA may suspend from the loan program those who take unfair advantage of veterans or discriminate because of race, color, religion, sex, disability, family status, or national origin. A significant benefit of military service is the VA home loan, allowing you to purchase a home with no down payment or refinance a home. If the lender charges discount points on the loan, the Veteran may negotiate with the seller as to who will pay points or if they will be split between buyer and seller. Points paid by the Veteran may not be included in the loan .

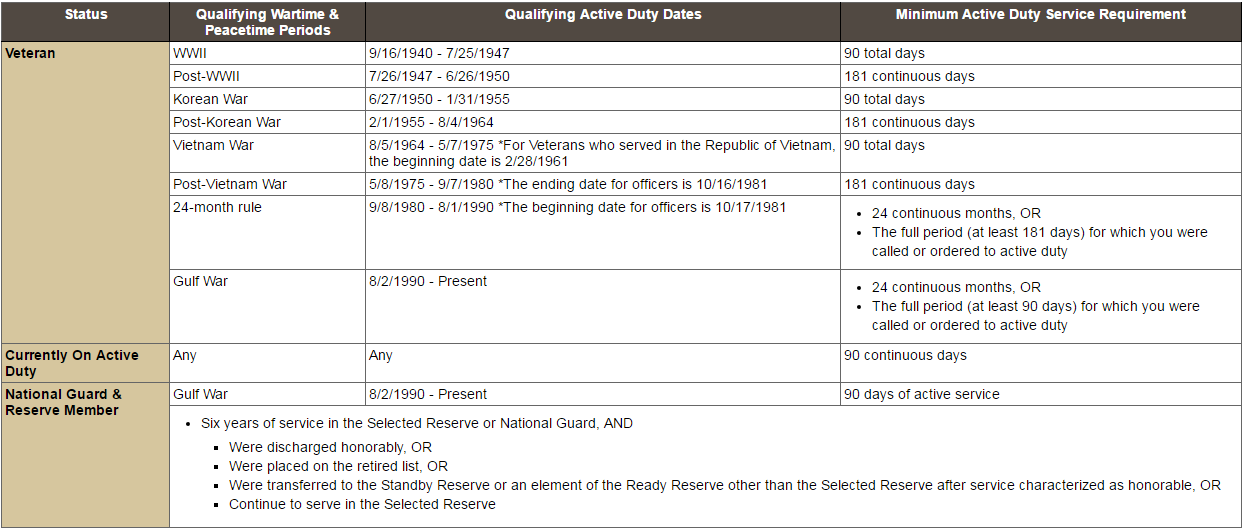

The program provides financing for purchases only, and cannot be used for refinancing. If you are now on regular duty , you are eligible after having served 181 days unless discharged or separated from a previous qualifying period of active duty service. Loans made prior to March 1, 1988, are generally freely assumable, but veterans should still request VA’s approval in order to be released of liability. However, for the entitlement to be restored, any loss suffered by VA must be paid in full. Let’s say the borrower is a veteran and wants a zero down VA home loan and is buying a first home.

To access the menus on this page please perform the following steps. To enter and activate the submenu links, hit the down arrow. You will now be able to tab or arrow up or down through the submenu options to access/activate the submenu links.

The VA has established lending guidelines that make it easier for a veteran or active duty service member to buy and finance a home to live in. Buyers don’t have to come up with a down payment which keeps many buyers on the sidelines longer when trying to save up enough money for a down payment and closing costs. Not having to jump over that hurdle is a big plus for veterans. An eligible borrower can use a VA-guaranteed Interest Rate Reduction Refinancing Loan to refinance an existing VA loan to lower the interest rate and payment.

Download the loan limit table by selecting the link to the right of the Description column. You can use your remaining entitlement—either on its own or together with a down payment—to take out another VA home loan. The borrower can prepay without penalty the entire loan or any part not less than one installment or $100. To understand the VA guarantee, one might think of VA loans in terms of small, medium and large. Before you buy, be sure to read the VA Home Loan Buyer's Guide. This guide can help you under the homebuying process and how to make the most of your VA loan benefit.Download the Buyer's Guide here.

No comments:

Post a Comment